Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

How Will the 2026 Federal Reserve Affect the Crypto Space?

Original Article Title: 2026: The Year of the Fed's Regime Change

Original Article Author: @krugermacro

Translation: Peggy, BlockBeats

Editor's Note: In 2026, the Federal Reserve may experience a true "regime change." If Hassett becomes the chair, monetary policy may shift from the Powell era's cautious approach to a more aggressive rate-cutting path and a "growth-first" framework. Short-term rates, long-term expectations, and cross-asset pricing will all be forced to reassess. This article outlines the key logic and market impact of this potential turning point. Next year's trading theme is not just about rate cuts but about a whole new Fed.

Below is the original text:

The Federal Reserve as we know it will come to an end in 2026.

The most important driver of asset returns next year will be the "New Fed" – more specifically, the policy paradigm shift brought about by a newly appointed chair by Trump.

Kevin Hassett has become the most likely candidate for Fed chair that Trump is likely to nominate (as of December 2, the Kalshi prediction market gives a 70% probability). Hassett is the current Director of the National Economic Council, a supply-side economist, and a long-time loyal supporter of Trump. He advocates for the idea of "growth first," believing that since the war against inflation has largely been won, maintaining high real interest rates is no longer economically rational but a politically stubborn stance. If he takes office, this will signify a decisive regime change: the Fed will shift from Powell's era of technocratic caution to a policy framework more explicitly aimed at lowering borrowing costs and advancing the president's economic agenda.

To understand the policy regime he will establish, one can look directly at his public statements this year on rates and the Fed:

"If the Fed doesn't cut rates in December, the only explanation is anti-Trump partisan bias." (November 21)

"If I were on the FOMC, I would be more likely to vote for a rate cut, while Powell would be less likely." (November 12)

"I agree with Trump: rates can be significantly lowered." (November 12)

"The expected three rate cuts are just the beginning." (October 17)

"I hope the Fed continues to aggressively cut rates." (October 2)

“The Fed's direction of interest rate cuts is correct, rates should be lower.” (September 18)

“Powell and Trump's views on rates are correct.” (June 23)

If the stance is mapped on a 1–10 scale from Dovish to Hawkish (1 = most Dovish, 10 = most Hawkish), Hassett is probably around 2.

If nominated, Hassett will take over Milan's position as a Fed Governor in January, as Milan's short term is due to end. Then in May, as Powell's term is up, he will be promoted to Chair; with Powell expected to resign his Governor seat after announcing his intent, creating a vacancy for Trump to nominate Warsh.

While Warsh is currently Hassett's main competitor for the Chair, this text assumes he will ultimately be assimilated into the system, acting as part of the reformist force. As a former Fed Governor, Warsh has been publicly “campaigning” for a platform of structural reform, explicitly calling for a reconstruction of a “new Treasury–Fed accord” and criticizing the current Fed leadership for “surrendering to the tyranny of the status quo.” Crucially, Warsh believes the current AI-driven productivity boom is inherently deflationary, implying that the Fed is making a policy error in maintaining a tightening stance.

New Power Equilibrium

In this architecture, the Trump version of the Fed will form a dominant dovish core team, with a viable path to securing votes on most easing issues. However, this is not a done deal, as consensus will still need to be reached, and the degree of dovishness is also uncertain.

➤ Dovish Core (4 individuals):

Hassett (Chair), Warsh (Governor), Waller (Governor), Bowman (Governor)

➤ Contestables (6 individuals):

Cook (Governor), Barr (Governor), Jefferson (Governor), Kashkari (Minneapolis), Williams (New York), A. Paulson (Philadelphia)

➤ Hawkish (2 individuals):

Hammack (Cleveland), Logan (Dallas)

However, if Powell chooses not to resign his Governor seat (though historically, it is highly unlikely—a departing Chair almost always resigns, e.g., Yellen resigned 18 days after Powell was nominated), that would be an extremely bearish scenario. Because this would not only block Warsh's vacancy, but also make Powell a “shadow Chair,” exerting stronger attraction and influence over the FOMC members outside the dovish core.

Timeline: Four Stages of Market Reaction

Based on all of the above factors, the market's reaction will generally go through four distinct stages:

1. (December / January of the following year) Immediate optimism after Haslett's nomination. In the weeks following confirmation, risk assets will welcome a new chair who is seen as decisive, dovish, and loyal.

2. If Powell does not announce his resignation within three weeks, a growing sense of unease will set in. Each day of delay will reactivate the tail risk of "what if he doesn't resign?"

3. When Powell announces his resignation, the market will see a wave of euphoria.

4. As the June 2026 FOMC meeting, chaired by Haslett for the first time, approaches, market sentiment will tense up again.

Investors will be highly attuned to all public remarks from FOMC members (who will speak frequently, providing clues to their thought processes and leanings).

Risk: A Divided Committee

In a scenario where the Chair's supposed "swing vote" (which doesn't actually exist) is not present, Haslett must win debates within the FOMC to secure a majority.

If every 50bp rate cut decision is only passed by a slim 7–5 margin, this will be erosive for institutions: signaling to the market that the Chair is more of a political proxy than an independent economist.

A more extreme scenario would be: a tie at 6–6, or a 4–8 vote against rate cuts

That would be catastrophic.

The specific voting details will be released in the FOMC meeting minutes three weeks after each meeting, making the minutes release a significant market-moving event.

As for what happens after the initial meeting, that remains a huge unknown.

My basic assessment is that with a stable support of 4 votes and a credible path to garnering 10 votes, Haslett will be able to shape a dovish consensus and advance his agenda.

Implication: The market cannot fully front-run the new Fed's dovish tilt.

Interest Rate Repricing

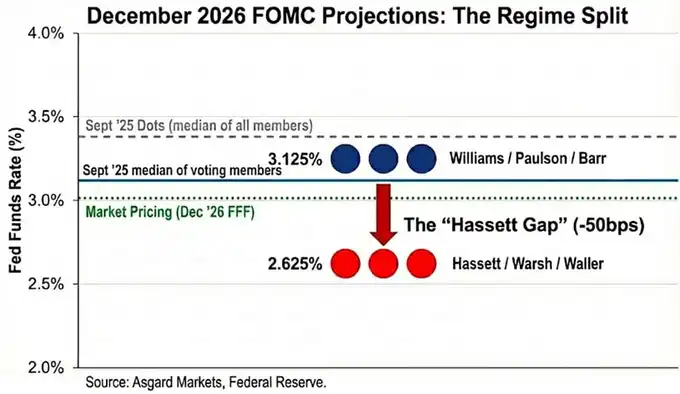

The "dot plot" is an illusion.

While the median forecast for the December 2026 interest rate released in September is 3.4%, this number represents the median of all participants (including non-voting hawkish members).

Based on attribution analysis of public remarks, I estimate that the true median of the voting members is significantly lower at 3.1%.

When replacing Powell and Milan with Hassett and Warsh, the picture changes further.

With Milan and Waller serving as proxies for a "dovish rate-cutting bias" new regime, the 2026 voting distribution still exhibits a bimodal shape, but both peaks are lower:

Williams / Paulson / Barr → 3.1%

Hassett / Warsh / Waller → 2.6%

I anchor the new leadership's target at 2.6% to align with Milan's official forecast; however, it is worth noting that Milan has publicly stated that the "neutral rate" should be between 2.0% and 2.5%, implying that the new regime's preference may be more dovish than indicated by the "dot plot".

The market has already begun to reflect this change, with the current (as of December 2nd) pricing for the December 2026 interest rate at 3.02%, but it has not fully priced in the upcoming regime shift. If Hassett successfully pushes the committee to further lower rates, the short end of the yield curve still has approximately 40 basis points of downside.

Furthermore, if Hassett's assessment of "Supply-Side Disinflation" is correct, inflation will decline faster than market consensus, forcing the Fed to cut rates further to avoid "passive tightening" due to rising real rates.

Cross-Asset Implications

While the market's initial reaction to Hassett's nomination should be "risk-on," a more precise characterization of this institutional transition is Reflationary Steepening:

Short end: Betting on aggressive rate cuts

Duration Play: Reflecting Higher Nominal Growth (and Inflation Risk)

1. Rates

Hasset's aim is to marry a “recessionary aggressive rate cut” with “3%+ boom-time growth.”

If this policy bears fruit: the 2-year yield will collapse to front-run the cuts; the 10-year yield could stay higher due to structural growth and higher inflation risk premium.

In simple words: front-end collapse, back-end resilience, and a steepening yield curve.

2. Equities

In Hasset's view, the current policy stance is suppressing AI-driven productivity booms.

Once in office: he would push down real discount rates, prompting growth stocks into a melt-up rally driven by valuation expansion.

The biggest risk is not a recession but a spike in the long end yields, possibly triggering a bond market “rebellion.”

3. Gold

When the Fed is politically in sync with the government and explicitly prioritizes growth over inflation targets, it is the classic bull case for hard assets.

Therefore: gold should outperform treasuries as markets hedge for a replay of the ‘70s-style “over-easing, policy error” in the new regime.

4. Bitcoin

Under normal circumstances, Bitcoin would be the purest expression of this “Regime Change” trade.

However, post the October 10 event, Bitcoin has exhibited: a clear downside skew; lackluster rallies in macro bullish times; cataclysmic drops in bearish times; fear of “four-year cycle tops”; a narrative identity crisis.

I believe that by 2026, Hasset’s monetary policy alongside Trump’s deregulatory agenda will be potent enough to override this self-reinforcing pessimism.

Tech Note: About Tealbook (Fed Internal Forecasts)

Tealbook is the official economic forecasting of the Fed research department and forms the statistical baseline for FOMC debates.

It is overseen by the Division of Research & Statistics, which has over 400 economists and is led by Director Tevlin.

Like most team members, Tevlin is a Keynesian, and the Fed's core model, FRB/US, is explicitly New Keynesian.

Hasset could appoint a supply-side economist to lead the division through a Board vote.

Replacing Keynesian modelers who "think growth will bring inflation" with supply-siders who "think AI prosperity will bring deflationary pressure" would significantly change forecasts.

For example, if the model predicts inflation will drop from 2.5% to 1.8% due to productivity gains,

those FOMC members who were not originally as dovish would also be more inclined to support aggressive rate cuts.

You may also like

Dragonfly Partners: Most agents will not engage in autonomous trading, how can crypto payments prevail?

US AI Startup Goes All In on Chinese Mega-Model | Rewire News Morning Brief

Trump Lies Again: A "Five-Day Pause" Psyop, How Wall Street, Bitcoin, and Polymarket Insiders Synced Uposciogen

When a Token Becomes Labor, People Become the Interface

Ceasefire News Leaked Ahead of Time? Large Polymarket Bets on Outcome Before Trump's Tweet

BlackRock CEO's Annual Shareholder Letter: How is Wall Street Using AI to Keep Profiting from National Pension Funds?

Sun Valley Releases 2025 Financial Report: Bitcoin Mining Revenue Reaches $670 Million, Accelerating Transformation to AI Infrastructure Platform

On March 16, 2026, in Dallas, Texas, USA, CanGu Company (New York Stock Exchange code: CANG, hereinafter referred to as "CanGu" or the "Company") today announced its unaudited financial performance for the fourth quarter and full year ended December 31, 2025. As a btc-42">bitcoin mining enterprise relying on a globally operated layout and dedicated to building an integrated energy and AI computing power platform, CanGu is actively advancing its business transformation and infrastructure development.

• Financial Performance:

Total revenue for the full year 2025 was $688.1 million, with $179.5 million in the fourth quarter.

Bitcoin mining business revenue for the full year was $675.5 million, with $172.4 million in the fourth quarter.

Full-year adjusted EBITDA was $24.5 million, while the fourth quarter was -$156.3 million.

• Mining Operations and Costs:

A total of 6,594.6 bitcoins were mined throughout the year, averaging 18.07 bitcoins per day; of which 1,718.3 bitcoins were mined in the fourth quarter, averaging 18.68 bitcoins per day.

The average mining cost for the full year (excluding miner depreciation) was $79,707 per bitcoin, and for the fourth quarter, it was $84,552;

The all-in sustaining costs were $97,272 and $106,251 per bitcoin, respectively.

As of the end of December 2025, the company has cumulatively produced 7,528.4 bitcoins since entering the bitcoin mining business.

• Strategic Progress:

The company has completed the termination of the American Depositary Receipt (ADR) program and transitioned to a direct listing on the NYSE to enhance information transparency and align with its strategic direction, with a long-term goal of expanding its investor base.

CEO Paul Yu stated: "2025 marked the company's first full year as a bitcoin mining enterprise, characterized by rapid execution and structural reshaping. We completed a comprehensive adjustment of our asset system and established a globally distributed mining network. Additionally, the company introduced a new management team, further strengthening our capabilities and competitive advantage in the digital asset and energy infrastructure space. The completion of the NYSE direct listing and USD pricing also signifies our transformation into a global AI infrastructure company."

"As we enter 2026, the company will continue to optimize its balance sheet structure and enhance operational efficiency and cost resilience through adjustments to the miner portfolio. At the same time, we are advancing our strategic transformation into an AI infrastructure provider. Leveraging EcoHash, we will utilize our capabilities in scalable computing power and energy networks to provide cost-effective AI inference solutions. The relevant site transformations and product development are progressing simultaneously, and the company is well-positioned to sustain its execution in the new phase."

The company's Chief Financial Officer, Michael Zhang, stated: "By 2025, the company is expected to achieve significant revenue growth through its scaled mining operations. Despite recording a net loss of $452.8 million from ongoing operations, mainly due to one-time transformation costs and market-driven fair value adjustments, the company, from a financial perspective, will reduce its leverage, optimize its Bitcoin reserve strategy and liquidity management, introduce new capital to strengthen its financial position, and seize investment opportunities in high-potential areas such as AI infrastructure while navigating market volatility."

The total revenue for the fourth quarter was $1.795 billion. Of this, the Bitcoin mining business contributed $1.724 billion in revenue, generating 1,718.3 Bitcoins during the quarter. Revenue from the international automobile trading business was $4.8 million.

The total operating costs and expenses for the fourth quarter amounted to $4.56 billion, primarily attributed to expenses related to the Bitcoin mining business, as well as impairment of mining machines and fair value losses on Bitcoin collateral receivables.

This includes:

· Cost of Revenue (excluding depreciation): $1.553 billion

· Cost of Revenue (depreciation): $38.1 million

· Operating Expenses: $9.9 million (including related-party expenses of $1.1 million)

· Mining Machine Impairment Loss: $81.4 million

· Fair Value Loss on Bitcoin Collateral Receivables: $171.4 million

The operating loss for the fourth quarter was $276.6 million, a significant increase from a loss of $0.7 million in the same period of 2024, primarily due to the downward trend in Bitcoin prices.

The net loss from ongoing operations was $285 million, compared to a net profit of $2.4 million in the same period last year.

The adjusted EBITDA was -$156.3 million, compared to $2.4 million in the same period last year.

The total revenue for the full year was $6.881 billion. Of this, the revenue from the Bitcoin mining business was $6.755 billion, with a total output of 6,594.6 Bitcoins for the year. Revenue from the international automobile trading business was $9.8 million.

The total annual operating costs and expenses amount to $1.1 billion.

Specifically, they include:

· Revenue Cost (excluding depreciation): $543.3 million

· Revenue Cost (depreciation): $116.6 million

· Operating Expenses: $28.9 million (including related-party expenses of $1.1 million)

· Miner Impairment Loss: $338.3 million

· Bitcoin Collateral Receivable Fair Value Change Loss: $96.5 million

The full-year operating loss is $437.1 million. The continuing operations net loss is $452.8 million, while in 2024, there was a net profit of $4.8 million.

The 2025 non-GAAP adjusted net profit is $24.5 million (compared to $5.7 million in 2024). This measure does not include share-based compensation expenses; refer to "Use of Non-GAAP Financial Measures" for details.

As of December 31, 2025, the company's key assets and liabilities are as follows:

· Cash and Cash Equivalents: $41.2 million

· Bitcoin Collateral Receivable (Non-current, related party): $663.0 million

· Miner Net Value: $248.7 million

· Long-Term Debt (related party): $557.6 million

In February 2026, the company sold 4,451 bitcoins and repaid a portion of related-party long-term debt to reduce financial leverage and optimize the asset-liability structure.

As per the stock repurchase plan disclosed on March 13, 2025, as of December 31, 2025, the company had repurchased a total of 890,155 shares of Class A common stock for approximately $1.2 million.

The US AI Startup Is Loving China's Open Source Model

Three Weeks of the US-Iran War: Who's Making Money, Who's Paying the Bill?

Interpreting Polymarket's Major Update Last Night: Fee Expansion, Self-Regulation, and New Incentives

From Human Application to Intelligent Collaboration: How GOAT Network Builds the Next Generation Digital Economy

CZ Washington Dialogue: Crypto Entrepreneurs are Accelerating Their Return to the United States

Morning Report | Strategy increased its holdings by 1,031 bitcoins last week; Katana Blockchain acquires IDEX; NYSE completes rule change to eliminate trading limits on crypto ETF options

Electric Capital: Tracking 501 types of yield-generating RWA assets, we discovered these patterns

Those who are cut off by AI will not disappear; they will become the creators of the next round of the economy

Stablecoins reshaping cross-border payments in Asia? Strategic panorama and investment opportunity analysis

Zuckerberg is building an AI agent to help him as CEO