Buy Crypto

Buy Crypto- Markets

Futures

Futures- Spot

- Copy Trade

- Earn

- More

Crypto ETF Fund Outflows: Is BlackRock and Other Issuers Still Making Money?

Original Article Title: When Wrappers Run Red

Original Article Author: Prathik Desai, Token Dispatch

Original Article Translation: Luffy, Foresight News

During the first two weeks of October 2025, Bitcoin spot ETFs saw inflows of $32 billion and $27 billion, setting records for the highest and fifth-highest weekly net inflows in 2025.

Prior to this, Bitcoin ETFs were on track to achieve a "no consecutive outflow week" milestone in the second half of 2025.

However, the most severe cryptocurrency liquidation event in history occurred unexpectedly. This event, which resulted in the evaporation of assets worth $190 billion, continues to haunt the crypto market.

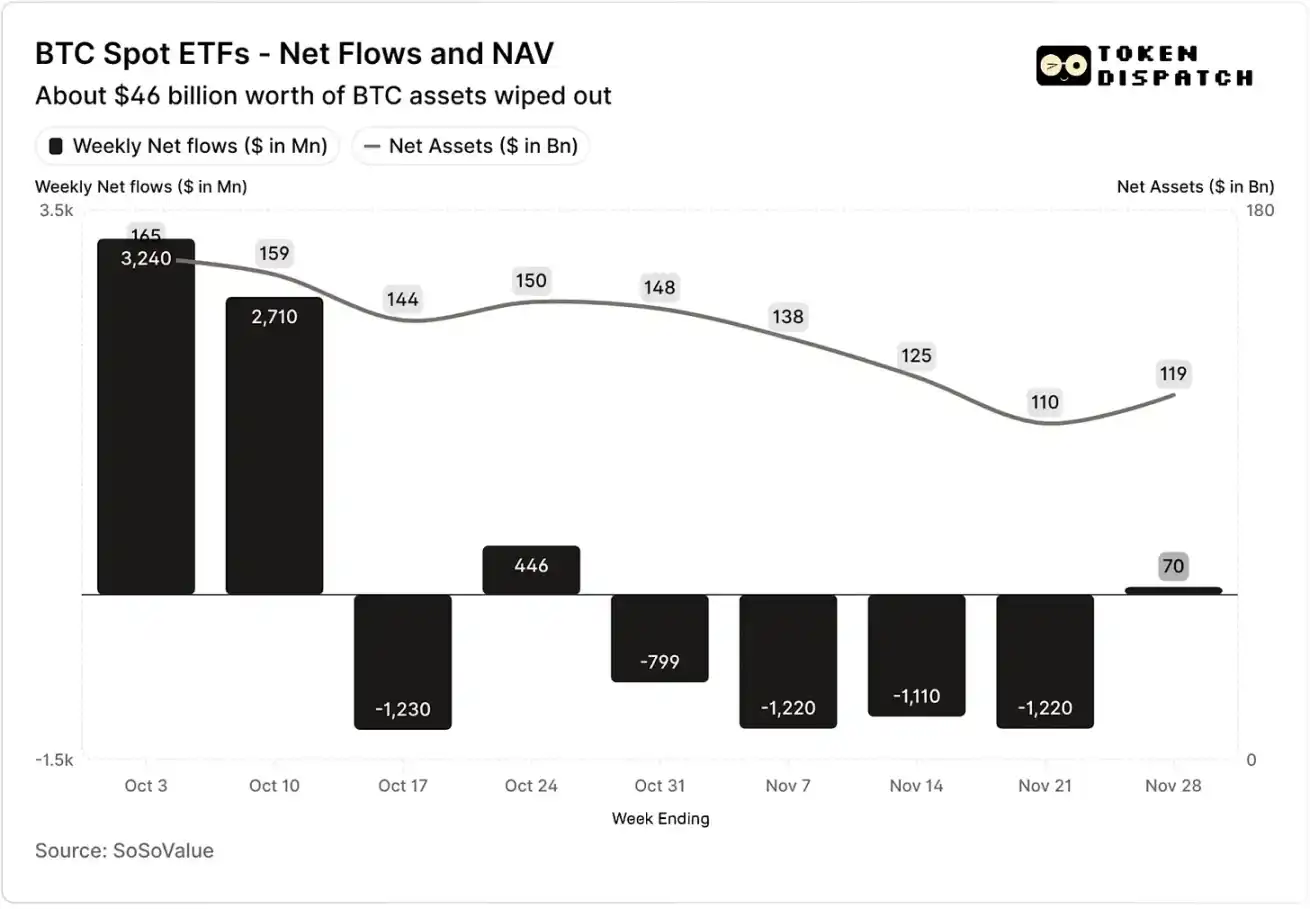

Net Fund Flows and Asset Net Value of Bitcoin Spot ETFs in October and November

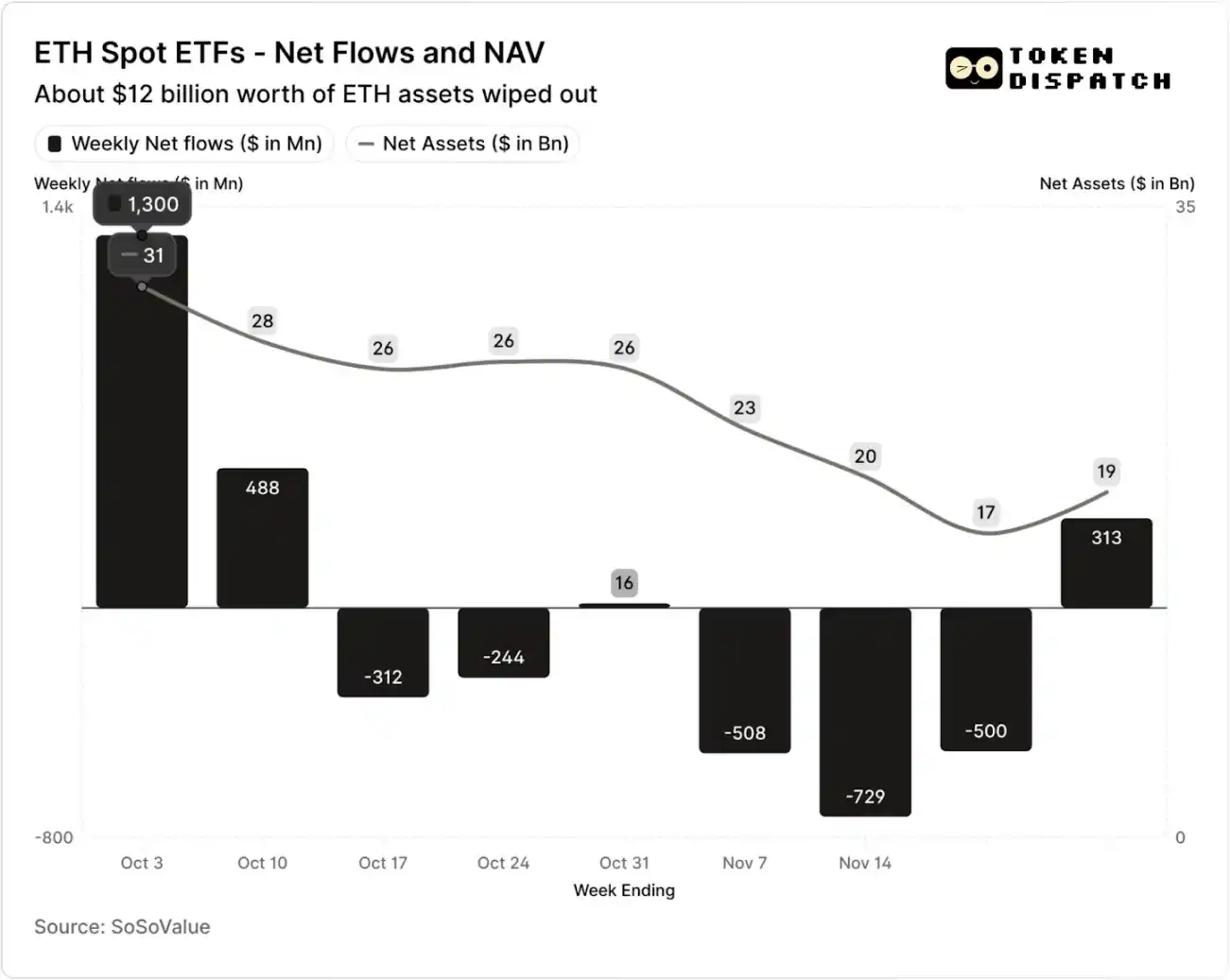

Net Fund Flows and Asset Net Value of Ethereum Spot ETFs in October and November

However, in the seven weeks following the liquidation event, Bitcoin and Ethereum ETFs experienced outflows in five weeks, totaling over $50 billion and $20 billion, respectively.

By the week ending November 21, the Net Asset Value (NAV) managed by the Bitcoin ETF issuer had shrunk from approximately $1.645 trillion to $1.101 trillion, while the Ethereum ETF's asset net value was nearly halved, dropping from $306 billion to $169 billion. This decline was partly due to the price decline of Bitcoin and Ethereum themselves, as well as some tokens being redeemed. In less than two months, the combined net asset value of Bitcoin and Ethereum ETFs evaporated by about one-third.

The retreat in fund flows reflects not only investor sentiment but also directly impacts the fee income of ETF issuers.

Bitcoin and Ethereum spot ETFs are the "money printers" of institutions like BlackRock, Fidelity, Grayscale, Bitwise, etc. Each fund charges fees based on the assets under management, typically expressed as an annual fee rate but actually accrued based on daily net asset value.

Every day, the trust funds holding Bitcoin or Ethereum shares will sell a portion of their holdings to cover transaction fees and other operational expenses. For the issuer, this means that their annual revenue is approximately equal to the Assets Under Management (AUM) multiplied by the fee rate; for the holders, this results in a gradual dilution of the amount of tokens held over time.

The fee rate range for ETF issuers is between 0.15% and 2.50%.

Redemption or outflows of funds themselves do not directly result in profit or loss for the issuer, but outflows cause a reduction in the issuer's ultimately managed asset size, thereby decreasing the asset base on which fees can be collected.

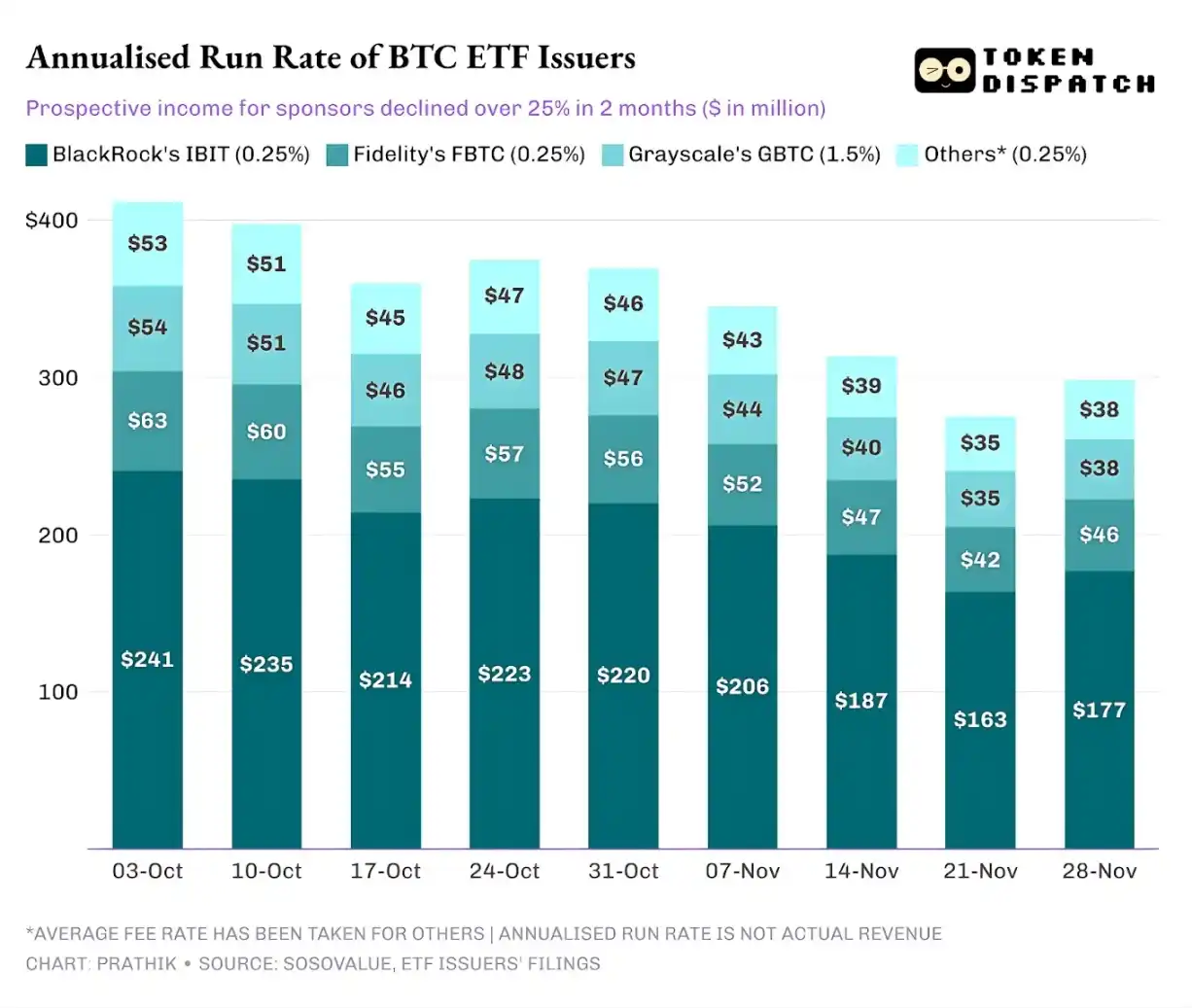

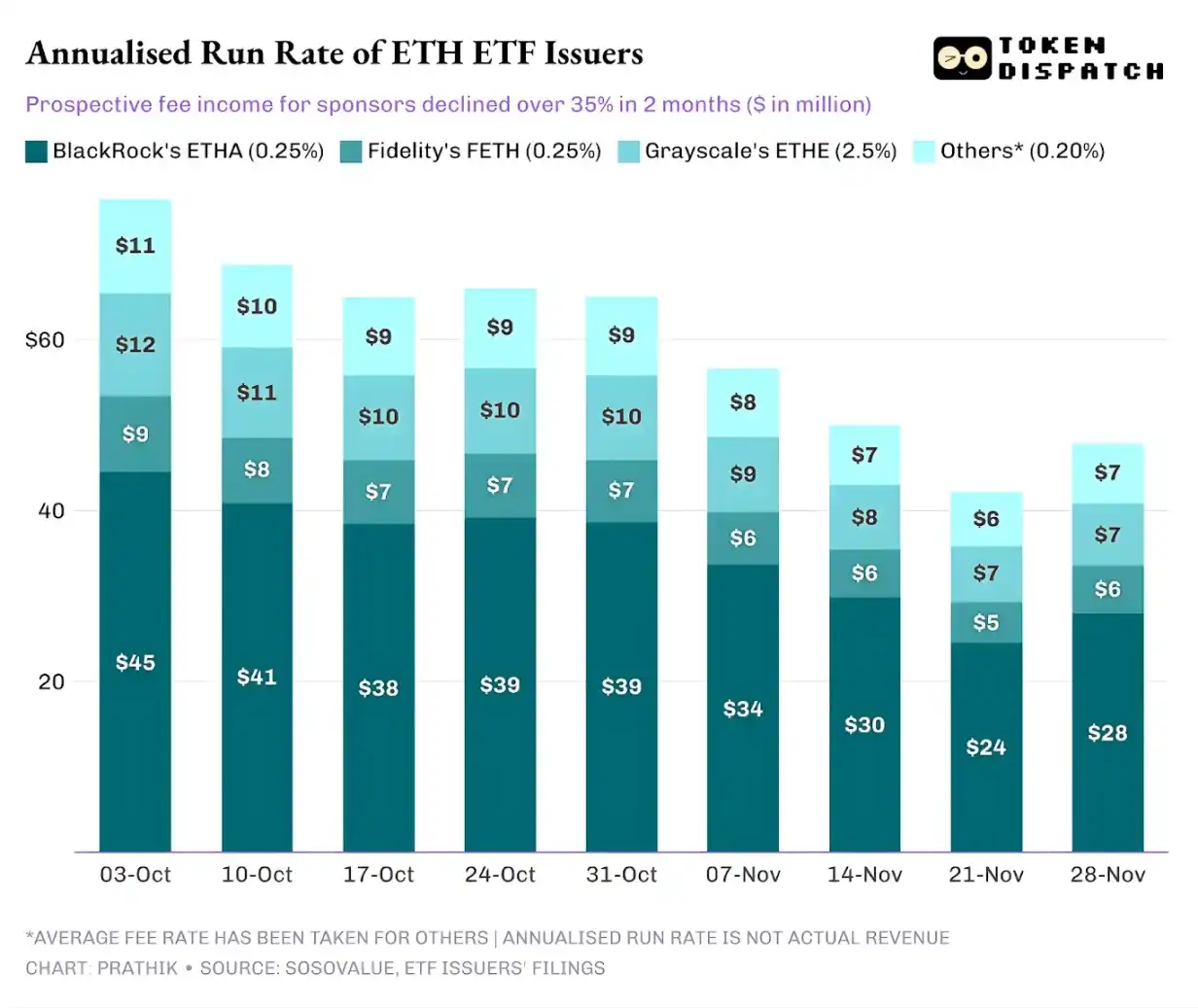

On October 3, the total assets under management by Bitcoin and Ethereum ETF issuers reached $195 billion, considering the aforementioned fee levels, their fee pool size was considerable. However, by November 21, the remaining asset size of these products was only about $127 billion.

If we calculate the annualized fee income based on the weekend's assets under management, over the past two months, the potential revenue for Bitcoin ETFs has declined by over 25%; Ethereum ETF issuers have been more significantly affected, with a 35% decline in annualized revenue over the past nine weeks.

The Larger the Issuance Scale, the Harder the Fall

From the perspective of a single issuer, there are three slightly different trends behind the flow of funds.

For BlackRock, its business characteristics involve a combination of "economies of scale" and "cyclical fluctuations." Its IBIT and ETHA have become the default choices for mainstream investors to allocate Bitcoin and Ethereum through an ETF channel. This has allowed the world's largest asset management institution to charge a 0.25% fee based on its large asset base, especially when the asset size hit a record in early October, the gains were substantial. However, this also means that when large holders decided to reduce risk in November, IBIT and ETHA became the most direct selling targets.

The data is sufficient to support this: BlackRock's Bitcoin and Ethereum ETFs saw annualized fee income declines of 28% and 38%, exceeding the industry average declines of 25% and 35%.

Vanguard's situation is similar to that of BlackRock, but on a relatively smaller scale. Its FBTC and FETH funds also followed the rhythm of "inflow first, outflow later," where the market enthusiasm in October was eventually replaced by outflows in November.

Grayscale's story is more about "historical legacy issues." Once upon a time, GBTC and ETHE were the only scaled channels for numerous U.S. investors to allocate Bitcoin and Ethereum through brokerage accounts. However, with institutions like BlackRock and Vanguard leading the market, Grayscale's monopoly position no longer exists. To make matters worse, the high fee structure of its early products has led to continued outflow pressure over the past two years.

The market performance in October and November also confirmed this investor tendency: when the market is bullish, funds will shift to lower-fee products; when the market weakens, positions will be significantly reduced.

The early Grayscale cryptocurrency products had a fee rate 6-10 times lower than low-cost ETFs. Although a high fee rate can boost revenue figures, the elevated cost will continuously drive investors away, diminishing the asset under management that generates fee income. The retained funds are often constrained by frictional costs such as taxation, investment mandates, operational processes, rather than stemming from active investor choices; and each outflow reminds the market: once a superior option arises, more holders will abandon high-fee products.

These ETF data unveil several key features of the current cryptocurrency institutionalization process.

The spot ETF market in October and November demonstrates that the cryptocurrency ETF management business is as cyclical as the underlying asset market. When asset prices rise and market sentiment is positive, inflows will drive up fee revenue; however, once the macro environment changes, funds will swiftly exit.

Although large issuance institutions have established efficient "fee channels" on Bitcoin and Ethereum assets, the volatility in October and November proves that these channels are also susceptible to market cycle impacts. For issuers, the core issue is how to retain assets in the face of a new market shock, avoiding significant fluctuations in fee revenue following macro trend changes.

While issuers cannot prevent investors from redeeming shares in a sell-off, income-generating products can to some extent mitigate downside risks.

Covered call option ETFs can provide investors with premium income (Note: A covered call option is an options trading strategy where an investor holds the underlying asset while simultaneously selling an equal number of call option contracts. Through collecting the premium, this strategy aims to enhance portfolio returns or hedge some risks.), offsetting some of the underlying asset price declines; collateralized products are also a viable direction. However, such products need to undergo regulatory review before being formally introduced to the market.

You may also like

Dragonfly Partners: Most agents will not engage in autonomous trading, how can crypto payments prevail?

US AI Startup Goes All In on Chinese Mega-Model | Rewire News Morning Brief

Trump Lies Again: A "Five-Day Pause" Psyop, How Wall Street, Bitcoin, and Polymarket Insiders Synced Uposciogen

When a Token Becomes Labor, People Become the Interface

Ceasefire News Leaked Ahead of Time? Large Polymarket Bets on Outcome Before Trump's Tweet

BlackRock CEO's Annual Shareholder Letter: How is Wall Street Using AI to Keep Profiting from National Pension Funds?

Sun Valley Releases 2025 Financial Report: Bitcoin Mining Revenue Reaches $670 Million, Accelerating Transformation to AI Infrastructure Platform

On March 16, 2026, in Dallas, Texas, USA, CanGu Company (New York Stock Exchange code: CANG, hereinafter referred to as "CanGu" or the "Company") today announced its unaudited financial performance for the fourth quarter and full year ended December 31, 2025. As a btc-42">bitcoin mining enterprise relying on a globally operated layout and dedicated to building an integrated energy and AI computing power platform, CanGu is actively advancing its business transformation and infrastructure development.

• Financial Performance:

Total revenue for the full year 2025 was $688.1 million, with $179.5 million in the fourth quarter.

Bitcoin mining business revenue for the full year was $675.5 million, with $172.4 million in the fourth quarter.

Full-year adjusted EBITDA was $24.5 million, while the fourth quarter was -$156.3 million.

• Mining Operations and Costs:

A total of 6,594.6 bitcoins were mined throughout the year, averaging 18.07 bitcoins per day; of which 1,718.3 bitcoins were mined in the fourth quarter, averaging 18.68 bitcoins per day.

The average mining cost for the full year (excluding miner depreciation) was $79,707 per bitcoin, and for the fourth quarter, it was $84,552;

The all-in sustaining costs were $97,272 and $106,251 per bitcoin, respectively.

As of the end of December 2025, the company has cumulatively produced 7,528.4 bitcoins since entering the bitcoin mining business.

• Strategic Progress:

The company has completed the termination of the American Depositary Receipt (ADR) program and transitioned to a direct listing on the NYSE to enhance information transparency and align with its strategic direction, with a long-term goal of expanding its investor base.

CEO Paul Yu stated: "2025 marked the company's first full year as a bitcoin mining enterprise, characterized by rapid execution and structural reshaping. We completed a comprehensive adjustment of our asset system and established a globally distributed mining network. Additionally, the company introduced a new management team, further strengthening our capabilities and competitive advantage in the digital asset and energy infrastructure space. The completion of the NYSE direct listing and USD pricing also signifies our transformation into a global AI infrastructure company."

"As we enter 2026, the company will continue to optimize its balance sheet structure and enhance operational efficiency and cost resilience through adjustments to the miner portfolio. At the same time, we are advancing our strategic transformation into an AI infrastructure provider. Leveraging EcoHash, we will utilize our capabilities in scalable computing power and energy networks to provide cost-effective AI inference solutions. The relevant site transformations and product development are progressing simultaneously, and the company is well-positioned to sustain its execution in the new phase."

The company's Chief Financial Officer, Michael Zhang, stated: "By 2025, the company is expected to achieve significant revenue growth through its scaled mining operations. Despite recording a net loss of $452.8 million from ongoing operations, mainly due to one-time transformation costs and market-driven fair value adjustments, the company, from a financial perspective, will reduce its leverage, optimize its Bitcoin reserve strategy and liquidity management, introduce new capital to strengthen its financial position, and seize investment opportunities in high-potential areas such as AI infrastructure while navigating market volatility."

The total revenue for the fourth quarter was $1.795 billion. Of this, the Bitcoin mining business contributed $1.724 billion in revenue, generating 1,718.3 Bitcoins during the quarter. Revenue from the international automobile trading business was $4.8 million.

The total operating costs and expenses for the fourth quarter amounted to $4.56 billion, primarily attributed to expenses related to the Bitcoin mining business, as well as impairment of mining machines and fair value losses on Bitcoin collateral receivables.

This includes:

· Cost of Revenue (excluding depreciation): $1.553 billion

· Cost of Revenue (depreciation): $38.1 million

· Operating Expenses: $9.9 million (including related-party expenses of $1.1 million)

· Mining Machine Impairment Loss: $81.4 million

· Fair Value Loss on Bitcoin Collateral Receivables: $171.4 million

The operating loss for the fourth quarter was $276.6 million, a significant increase from a loss of $0.7 million in the same period of 2024, primarily due to the downward trend in Bitcoin prices.

The net loss from ongoing operations was $285 million, compared to a net profit of $2.4 million in the same period last year.

The adjusted EBITDA was -$156.3 million, compared to $2.4 million in the same period last year.

The total revenue for the full year was $6.881 billion. Of this, the revenue from the Bitcoin mining business was $6.755 billion, with a total output of 6,594.6 Bitcoins for the year. Revenue from the international automobile trading business was $9.8 million.

The total annual operating costs and expenses amount to $1.1 billion.

Specifically, they include:

· Revenue Cost (excluding depreciation): $543.3 million

· Revenue Cost (depreciation): $116.6 million

· Operating Expenses: $28.9 million (including related-party expenses of $1.1 million)

· Miner Impairment Loss: $338.3 million

· Bitcoin Collateral Receivable Fair Value Change Loss: $96.5 million

The full-year operating loss is $437.1 million. The continuing operations net loss is $452.8 million, while in 2024, there was a net profit of $4.8 million.

The 2025 non-GAAP adjusted net profit is $24.5 million (compared to $5.7 million in 2024). This measure does not include share-based compensation expenses; refer to "Use of Non-GAAP Financial Measures" for details.

As of December 31, 2025, the company's key assets and liabilities are as follows:

· Cash and Cash Equivalents: $41.2 million

· Bitcoin Collateral Receivable (Non-current, related party): $663.0 million

· Miner Net Value: $248.7 million

· Long-Term Debt (related party): $557.6 million

In February 2026, the company sold 4,451 bitcoins and repaid a portion of related-party long-term debt to reduce financial leverage and optimize the asset-liability structure.

As per the stock repurchase plan disclosed on March 13, 2025, as of December 31, 2025, the company had repurchased a total of 890,155 shares of Class A common stock for approximately $1.2 million.

The US AI Startup Is Loving China's Open Source Model

Three Weeks of the US-Iran War: Who's Making Money, Who's Paying the Bill?

Interpreting Polymarket's Major Update Last Night: Fee Expansion, Self-Regulation, and New Incentives

From Human Application to Intelligent Collaboration: How GOAT Network Builds the Next Generation Digital Economy

CZ Washington Dialogue: Crypto Entrepreneurs are Accelerating Their Return to the United States

Morning Report | Strategy increased its holdings by 1,031 bitcoins last week; Katana Blockchain acquires IDEX; NYSE completes rule change to eliminate trading limits on crypto ETF options

Electric Capital: Tracking 501 types of yield-generating RWA assets, we discovered these patterns

Those who are cut off by AI will not disappear; they will become the creators of the next round of the economy

Stablecoins reshaping cross-border payments in Asia? Strategic panorama and investment opportunity analysis

Zuckerberg is building an AI agent to help him as CEO